The False Link Between Higher Stocks And A Stronger Economy

Disclosure: I have no positions in any stocks mentioned, and

no plans to initiate any positions within the next 72 hours.

It is hard to turn away from the financial news cycle. Of late, the purveyors

of news and commentary have quieted discussions regarding how Quantitative

Easing could be the culprit of higher stock prices and instead are going public

with the narrative that stock prices are going higher because the economic data

are good and getting so much better. Below are a sprinkling of data points that

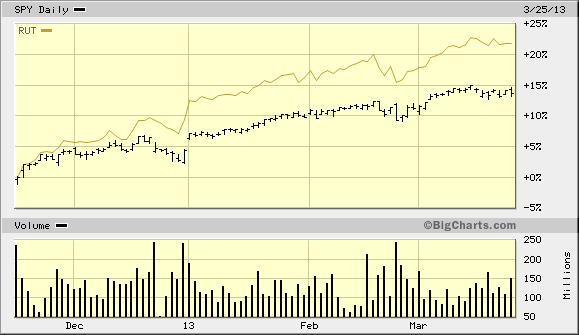

highlight why I am skeptical of this new found view.Skeptical that the economy is strong and strengthening and skeptical that the parabolic move in stock indexes since the end of November is grounded in reality at all. Since hitting a low of 1,343 on November 16, 2012, the S&P 500 (SPY) has rallied greater than 15% while the Russell 2000 (IWM) has rallied 23% in the same period.

(click to enlarge)

Looking at the new homebuilding numbers below, you can see that while new home sales are up over the prior year, the trend has not accelerated at all since the market began its ascent. Additionally, market participants should take notice that while the Western region of the U.S. saw new home sales rise greater than 50%, the next strongest region experienced a more modest 18% increase, while the remaining two regions saw a decline in building conditions. This uneven geographic distribution of new home sales is not characteristic of a housing market firing on cylinders.

Annualized New Home Sales

| U.S. | Northeast | MidWest | South | West | Inventories (Months) | |

| Feb-12 | 366 | 29 | 49 | 197 | 91 | 4.8 |

| November | 394 | 33 | 43 | 219 | 99 | 4.5 |

| December | 381 | 29 | 45 | 211 | 96 | 4.8 |

| Jan-13 | 431 | 30 | 51 | 206 | 144 | 4.2 |

| February | 411 | 26 | 58 | 186 | 141 | 4.4 |

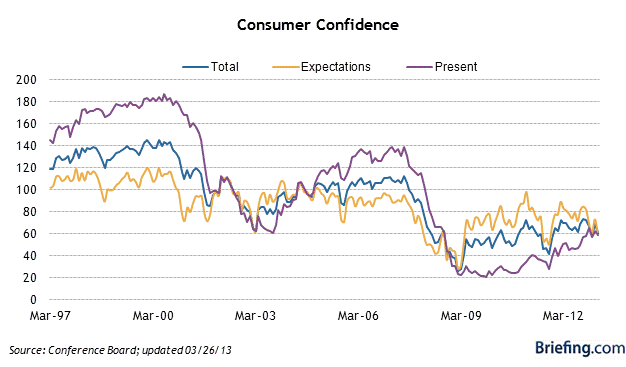

The consumer confidence numbers show an even more precarious picture as they are down both from November of 2012 and over the prior year. The NFIB optimism index, which measures the confidence of small business (which creates approximately 70% of jobs), similarly does not breed optimism. Apparently, while investors and speculators are partying like it's 1999 and 2000, the rest of the country is shrugging their shoulders in disbelief. As you can see from the chart below, consumer confidence is still 50%-100% away from where it typically is during economic expansion.

Consumer Confidence Table

* Data from Conference Board

(click to enlarge)

NFIB Optimism Index

| Feb | Jan 2013 | Dec | Nov | Feb 2012 | |

| Optimism Index | 90.8 | 88.9 | 88.0 | 87.5 | 94.3 |

While personal income has been flat from October 2012-January 2013 (the latest data), personal consumption is up 0.7% in the same period, indicating that consumers are borrowing money in order to spend. This is also reflected in the Federal Reserve's statistic of consumer credit, which increased $47.4 billion from November 2012-January 2013, though the federal government loaning money to students accounted for 2/3 of the increase. This implies that the expansion in consumer credit on its own is contributing more than a full percentage point to GDP on an annual basis. With unemployment still at recessionary levels, I wouldn't count on banks to get carried away with lending practices. Personal savings rate, meanwhile, is at its lowest level since November of 2007. Higher debt levels and lower savings appear to be end goals for the Federal Reserve, however, the low savings rate, currently 2.4%, leaves no room for consumers to react during the next recession, which leaves the door open for the government having to bail its people out in the future...if it still is able to do so by then.

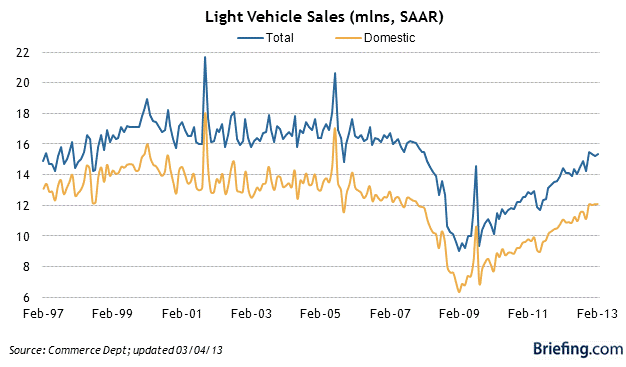

Meanwhile, light vehicle sales, a bright spot for the economy since 2009, have stalled out since November at an annualized pace of 15.5 million annually. This is likely in reaction to consumers waiting to see what was going to happen with payroll taxes and the sequester.

(click to enlarge)

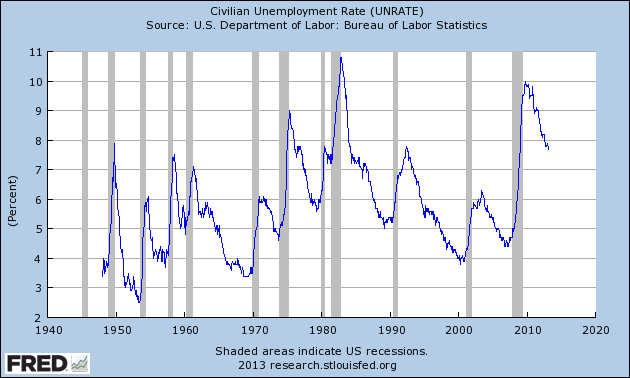

On the employment front, from November - February, the unemployment rate has decreased a scant 0.1%. The underemployment rate (U-6) similarly decreased 0.1% during the same period. At this rate it would take 4 years to get to the unemployment rate that the Federal Reserve has announced that it would find acceptable to turn less dovish in its monetary policy stance. In fact, the unemployment rate remains at or higher than the peak of seven of the past nine recessions.

(click to enlarge)

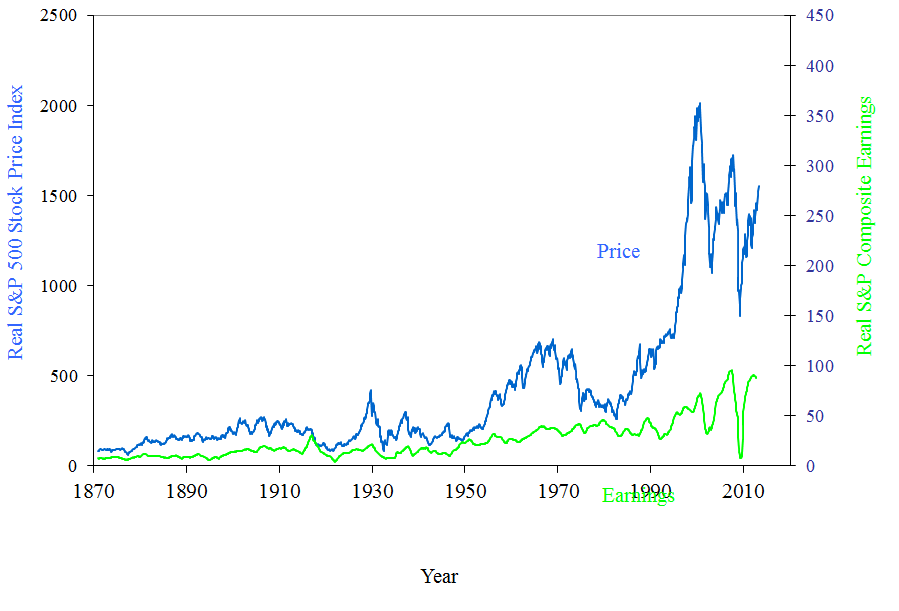

Meanwhile, when it comes to corporate earnings, famed economist Robert Shiller's chart shows that the correlation between price and earnings has nearly disappeared in recent history. I bring this up because while earnings in the S&P 500 have stalled out since the summer of 2011, stocks keep charging higher. There's nothing to say that this couldn't happen indefinitely, but the question is whether it is worth the risk.

(click to enlarge)

* Data from Robert Shiller

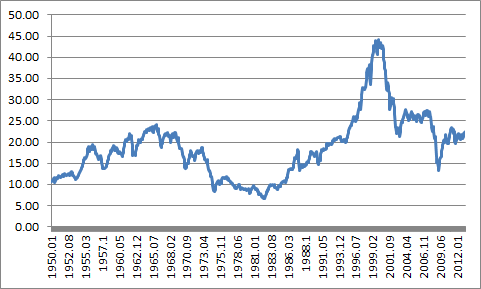

A look at the cyclically adjusted P/E ratio of the S&P might illustrate a different point depending on who's looking at it. I included two charts, one to remove the unlikely repeat of 1999. In the first chart, if you think that 1999 is repeatable, one would argue that the S&P 500 could double again...

Cyclically Adjusted P/E Ratio of S&P

(click to enlarge)

* Data from Robert Shiller

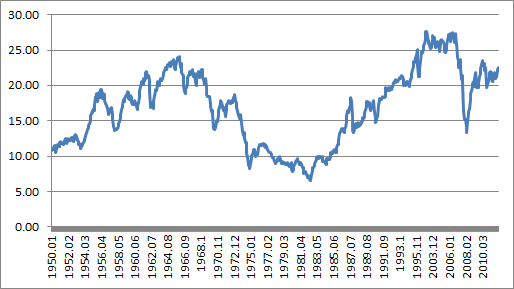

A look at the second chart, however, tells a different story. With the P/E currently around 23x and the high around 26x (and little real earnings growth expected), the best an investor could hope for over the 12-18 months is an additional 11%. With the average P/E in the below chart at 17x (and the real potential of a recession) the potential downside is at least 26%.

Cyclically Adjusted P/E Ratio of S&P (Adjusted to Exclude Internet Bubble)

(click to enlarge)

* Data from Robert Shiller

In conclusion, it appears from the data that the markets have completely disconnected from the reality of corporate earnings and the real economy. On top of the economic data being nothing to get excited about, there are numerous headwinds in the economy including the effects the sequester will have on millions of families, the payroll tax increase, the taxes associated with the affordable care act and a lack of liquidity among consumers. Additionally, companies cannot be expected to gain much more productivity, as they have already gone through rounds of layoffs during the great recession. When combined with the difficulties Europe is experiencing, it's difficult to see a clear line of path for sales and earnings growth that would justify the recent rally.

Disclosure: I have been skeptical about the economy and the markets since September of 2009. In my opinion, the Federal Reserve is inducing an interest rate driven bond bubble. More on this topic in a soon to come article.

and 235,800 people who get

Macro

View daily.

More articles by Paul Nouri »

- The Fed Controls Interest Rates... For Now Wed, Mar 27

- If Quest Returns To Its Core Strengths, It Can Deliver Big Returns For Shareholders Thu, Mar 21

- Enzo Investors Have To Be In It For The Long Haul Wed, Mar 20

- After Nearly Doubling In 2 Months, Shares Of Best Buy Appear To Trade At Fair Value Tue, Mar 19

No comments:

Post a Comment